SVB seized by FDIC, Signature bank falls in heavy trade as bitcoin breaks down | Opinion

The views and opinions expressed here belong solely to the author.

Niche banks continue to fall apart. The Silvergate failure is being followed by Silicon Valley Bank (SVB), which collapsed on March 10.

After a failed attempt to raise capital, SBV has been taken over by the Federal Deposit Insurance Corporation (FDIC). The bank will be sold or liquidated.

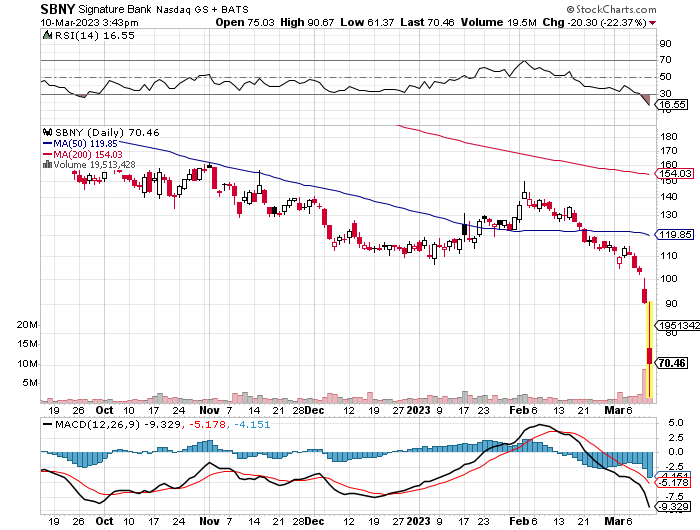

In heavy trade on March 10, Signature Bank is on the rocks. It is down 21.11% at press time at $69.65, but traded near $61 earlier in the day from a previous close of $90.76. Much like SVB did earlier in the week, Signature is denying that it has any capital issues.

Signature Bank Share Price | Source: StockCharts.com

While these banks are small, the impact they are having on global markets is noticeable.

According to a recent disclosure, Circle held money with SVB, which only makes the ongoing stablecoin reserves saga more complex. Because SVB is now in FDIC control, the process of winding up the bank or selling it should be quickly, but until it is done, whatever reserves Circle had with SVB are frozen.

JUST IN: Circle $USDC held an undisclosed amount of cash in Silicon Valley Bank $SIVB. pic.twitter.com/0U1iKTUS08

— Watcher.Guru (@WatcherGuru) March 10, 2023

None of this is good for cryptos, which are both emerging fintech, and a volatile asset.

Cryptos have come under strong selling pressure, with bitcoin falling below $20,000 for the first time since January. There is little doubt that the crypto markets are directly linked to capital flows in the legacy financial system, and in fact, cryptos may be a leading indicator for the direction of risk assets in the wider world of finance.

An ocean of liquidity, for some

Any market thrives or dies on access to liquidity, and cryptos are no different. On March 10, John Wu, the president of Ava Labs, said he thought that the SVB fiasco was a bank run. He turned out to be correct. SVB was not a risky bank, but as soon as people smell blood in the water, bad things can happen.

Many people in the legacy financial markets either remember, or have learned about the 2008 Lehman Brothers disaster. What many don’t recall is that the seeds of the crisis were planted a year earlier, when BNP Paribas suspended trade in some of its funds.

The reason behind the suspension of trade was that the BNP funds held subprime U.S. mortgage bonds.

According to the bank, as these funds were largely illiquid, there was no market-making mechanism to value them, and thus, they could not be valued. In the absence of a buyer, the value of the subprime bonds was effectively zero.

Today, as small banks and risk assets sell off hard, there are many questions that remain in the marketplace. Both Silvergate and SVB had huge exposure to both tech, and startups. Assets in the tech startup and VC space, much like the subprime mortgage bond market of 2008, are largely illiquid.

Shares in small companies aren’t traded with a market-making mechanism, and there is no centralized price-setting exchange. In the crypto space, the problems with valuation grow. In most cases a token isn’t equity. As one analyst noted, token are like tickets to a carnival, not ownership of the carnival itself.

As liquidity evaporates, and a flight-to-quality trade emerges, this lack of equity may become an Achilles heel for the blockchain development space.

The no-ownership culture

The idea behind bitcoin was decentralization, and as a result, many blockchains that exist today don’t have owners. You can use the platform, but in one way or the other, you can’t own it. When times get hard, and liquidity dries up, this makes raising funds difficult.

Some platforms have token reserves for this purpose, but many don’t. When a company gets into trouble, and needs money, it can sell equity. While many people think about tokens like stock, in most cases, it isn’t.

Of course, there are companies in the blockchain space that do have a corporate structure, but like most startups, they are small companies that place shares in fund raising rounds with venture capitalists, and these shares are generally illiquid investments.

When times are good, these private shares are easy to sell, but in a rough market, like sub-prime bonds, they may as well be worthless.

A company that can’t take on debt, or sell equity, has to rely on revenue to fund its operations. For many early-stage tech companies, this simply isn’t an option. In a worst case scenario, the emerging tech sector could implode, and the IP generated will be put out on the market at fire sale prices.

What does the abyss look like?

There is no organic liquidity in the blockchain space from a fiat perspective.

Fiat money flows into crypto and blockchain in two main channels. Either it comes from retail investors, or institutional investors. While more people are willing to accept cryptos as a means of payment all the time, as prices decline in fiat terms, that trade becomes less attractive from a fiat point of view.

Institutional investors who embraced bitcoin, like Microstrategy’s Michael Saylor, have faced severe consequences. Then there is the reputational risk that cryptos pose to institutional investors. If a industry leader like Charlie Munger or Jamie Dimon finds out a CEO is into bitcoin, there could be hardships as a result.

The last time bitcoin and crypto faced a prolonged bear market, it was a different industry. PayPal was blocking anyone who was near crypto, and the idea that major banks would offer crypto custody services was absurd.

Now, big money is looking for good deals. Smart money bought Apple Computer shares at $2 a share after the dot-com collapse. The same smart money will be looking for distressed assets in 2023, and given the market conditions, that money will be spoiled for choice.

About the author: Nicholas Say is the news editor at crypto.news. While be began his working life in visual arts, he loves to write. Nicholas thinks that words pack more power than images, and are far more precise. Given the choice between dogs and cats, Nicholas prefers dogs, but not by a wide margin. He has worked in a writing or editing capacity at a number of companies, including Blockonomi, and Grit Daily. When he isn’t working, Nicholas loves to cook.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  USDC

USDC  Dogecoin

Dogecoin  Cardano

Cardano  Bitcoin Cash

Bitcoin Cash  LEO Token

LEO Token  Stellar

Stellar  Litecoin

Litecoin  Hedera

Hedera  OKB

OKB  Gate

Gate  Cosmos Hub

Cosmos Hub  VeChain

VeChain  Algorand

Algorand  KuCoin

KuCoin  Tether Gold

Tether Gold  Zcash

Zcash  IOTA

IOTA  TrueUSD

TrueUSD  NEO

NEO  Polygon

Polygon  Decred

Decred  Ravencoin

Ravencoin  Synthetix Network

Synthetix Network  Basic Attention

Basic Attention  0x Protocol

0x Protocol  Siacoin

Siacoin  Holo

Holo  DigiByte

DigiByte  Enjin Coin

Enjin Coin  Nano

Nano  Ontology

Ontology  Status

Status  Waves

Waves  Pax Dollar

Pax Dollar  Steem

Steem  BUSD

BUSD  Numeraire

Numeraire  OMG Network

OMG Network  Ren

Ren  HUSD

HUSD  Augur

Augur