US Banking Industry in Turmoil: A Comprehensive Look at the ‘Great Consolidation’ and Largest Bank Failures of 2023

2023 has been a rollercoaster ride for the U.S. banking industry. The collapse of three major banks has sent shockwaves through the financial world, with their combined assets surpassing the top 25 banks that crumbled in 2008. The following is a closer look at what has triggered a ‘great consolidation’ in the banking sector, a recurring theme in the industry’s history over the past century.

A Listicle of Bank Consolidation, Failures, and Issues Facing the U.S. Banking Sector

The U.S. banking industry has taken a beating in 2023, with the market capitalizations of dozens of banks across the country dropping considerably in recent months. The reasons for this struggle are varied, with some blaming poor choices by financial institutions and others pointing fingers at the U.S. central bank. While it’s important to consider different opinions, a comprehensive listicle of information can shed light on the country’s ‘great consolidation’ in the banking sector and the largest bank failures in the United States. So, let’s take a closer look at these developments and what they mean for the country’s banking industry.

- In the year 1920, historical data reveals that the United States boasted a grand total of approximately 31,000 banks. However, by the year 1929, this number had dwindled down to less than 26,000. Since that time, the number of banks has experienced a precipitous decline, plummeting by a staggering 84%. As a result, fewer than 4,160 banks remain in operation today.

- Out of the 4,150 U.S. banks, the top ten hold more than 54% of FDIC-insured deposits. The four largest banks in the country have amassed a whopping $211.5 billion in unrealized losses, with Bank of America bearing the brunt of a third of that amount.

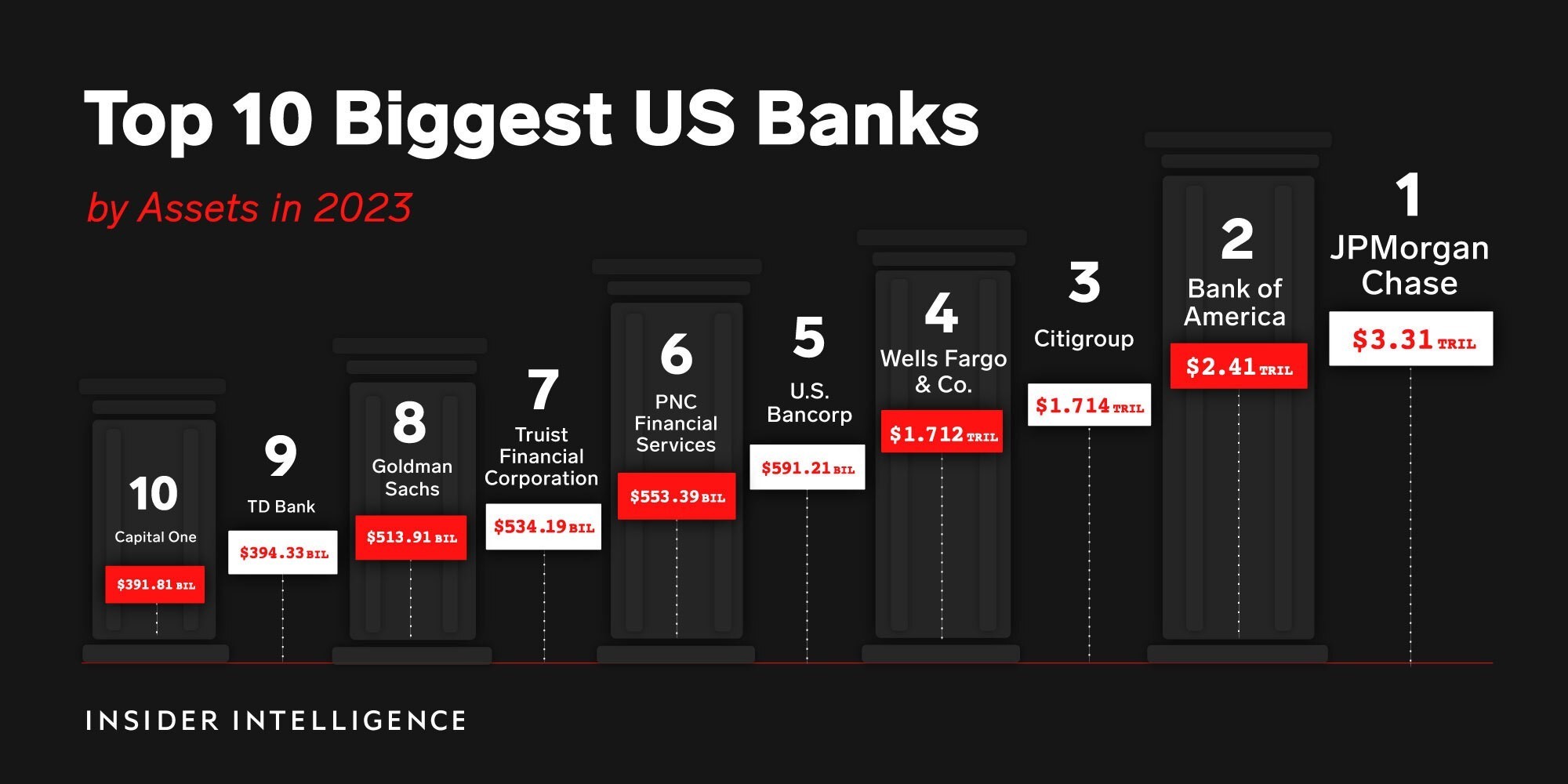

The top ten largest U.S banks by assets in 2023 according to Insider Intelligence.

- A recent Stanford study shows U.S. banks collectively had $1.7 trillion in unrealized losses at the end of 2022 which is awfully close to their total equity of $2.1 trillion. American banks also hold nearly $1.5 trillion in debt, which is due by the end of 2025. American financial institutions have also amassed a significant amount of commercial real estate that’s been decreasing in value.

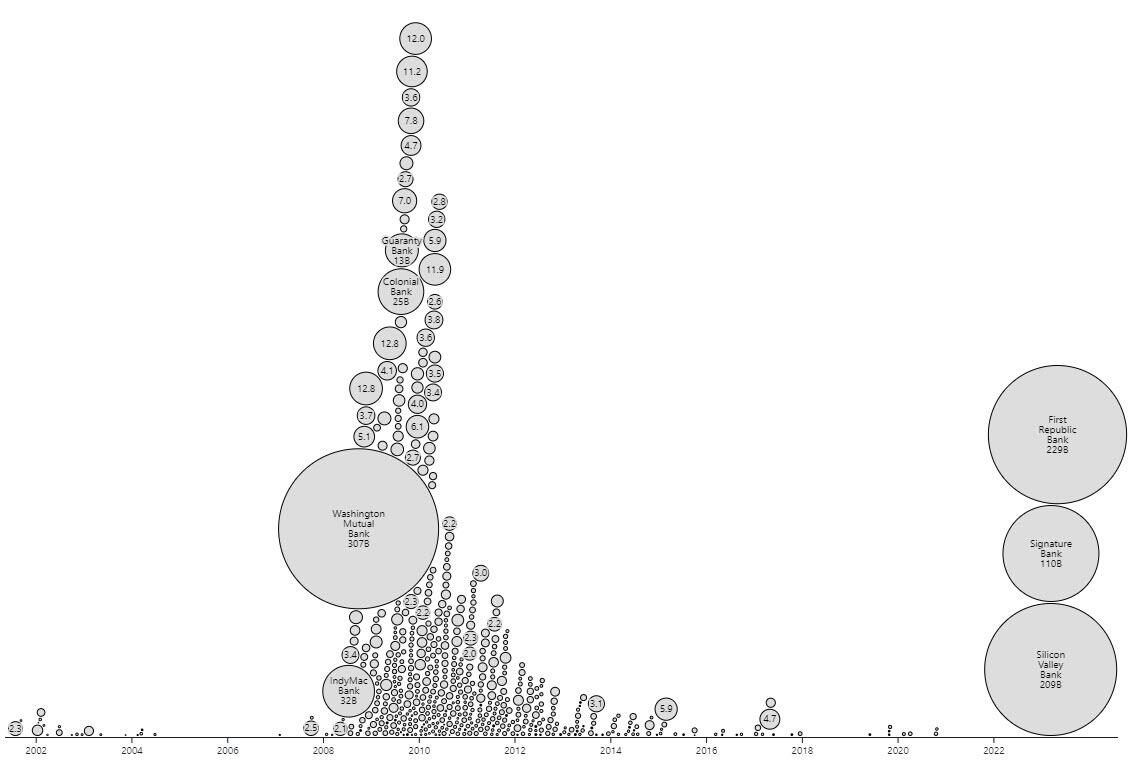

- The collapse of First Republic Bank, Silicon Valley Bank, and Signature Bank were the third, fourth, and fifth largest bank failures in the United States. Data shows the combined assets of all three banks outpaced the top 25 bank failures of 2008.

The combined assets of First Republic Bank, Silicon Valley Bank, and Signature Bank outpaced the top 25 bank failures in 2008.

- The Federal Deposit Insurance Corporation (FDIC) provided JPMorgan Chase a $50 billion credit line and noted it lost $13 billion from the First Republic Bank fallout. The FDIC estimated the cost of Signature Bank’s failure to its Deposit Insurance Fund to be around $2.5 billion and the Silicon Valley Bank collapse cost the FDIC $20 billion, bringing the total to $35.5 billion.

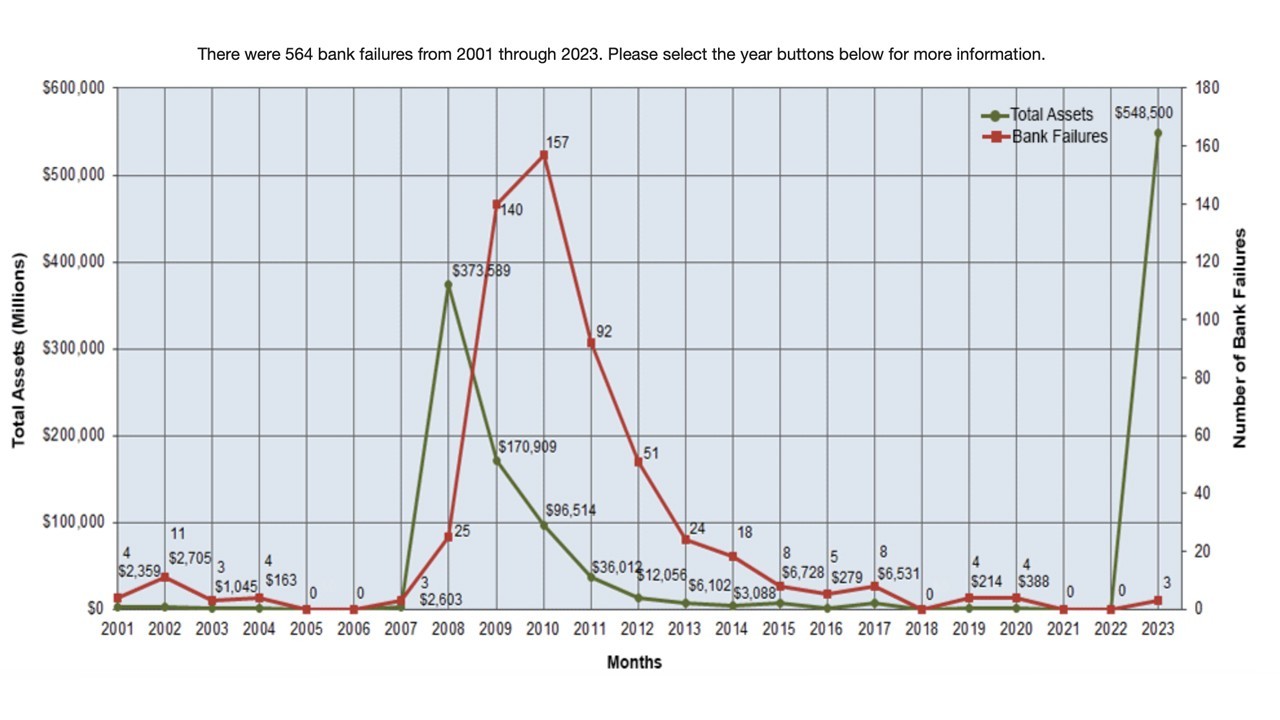

A look at the largest bank failures in the United States since 2002.

- In addition to the recent First Republic Bank collapse, Pacwest Bancorp’s shares have been sinking steeply. Over the past six months, Pacwest has lost 73% of its market capitalization value. Presently, Pacwest is weighing strategic options and a possible sale, according to people familiar with the matter.

- Western Alliance Bancorp is also struggling with shares down 57% lower during the last six months. While several of the failed banks saw significant withdrawals like First Republic’s $100 billion outflow in March, Western Alliance claims it has not seen any unusual deposit outflows.

- Sources and statistics show that U.S. banks that provide mortgages lost an average of $301 for every loan that originated in 2022, down 87.13% from the $2,339 profit per loan in 2021.

- In the second quarter of 2021, banks acquired a record amount of government debt by obtaining $150 billion worth of 10-year Treasury notes. However, thanks to the Fed’s ten consecutive rate hikes, 10-year and 2-year treasury bonds in the U.S. are currently inverted. This means the banks with excessive reliance on long term bonds are struggling because the yields on the 2-year Treasury note are actually higher than the 10-year Treasury.

- On May 3, 2023, the U.S. Federal Reserve raised the benchmark bank rate and it is now at a 16-year high.

- In March, the four biggest U.S. banks by assets held, JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo collectively lost $52 billion of market value.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  USDC

USDC  Dogecoin

Dogecoin  Cardano

Cardano  Bitcoin Cash

Bitcoin Cash  LEO Token

LEO Token  Stellar

Stellar  Litecoin

Litecoin  Zcash

Zcash  Hedera

Hedera  Tether Gold

Tether Gold  OKB

OKB  KuCoin

KuCoin  Cosmos Hub

Cosmos Hub  Algorand

Algorand  Gate

Gate  VeChain

VeChain  TrueUSD

TrueUSD  IOTA

IOTA  Basic Attention

Basic Attention  NEO

NEO  Decred

Decred  Synthetix

Synthetix  Ravencoin

Ravencoin  0x Protocol

0x Protocol  DigiByte

DigiByte  Nano

Nano  Siacoin

Siacoin  Numeraire

Numeraire  Waves

Waves  Status

Status  Ontology

Ontology  Enjin Coin

Enjin Coin  BUSD

BUSD  Pax Dollar

Pax Dollar  Steem

Steem  OMG Network

OMG Network  Augur

Augur  Bitcoin Diamond

Bitcoin Diamond